Python Trading Bot

The 50-SMA is a super popular trading indicator for quantitative trading analysis. With the ongoing maturation of the general crypto market and the explosion of crypto trading bots, I thought it would be a great time to share how simple it is to calculate the SMA for yourself.

Using this article, you can easily plug the indicator into your trading bot. I’ll be using Python 3, Python Panda’s, and data from Binance. Links to these resources can be found at the bottom of the article.

What is an SMA?

SMA is the acronym for a ‘Simple Moving Average’. It is the average price over a determined number of periods. The indicator is often used by traders to help predict trends in the market, with 50-day, 100-day, and 200-day indicators being the most common.

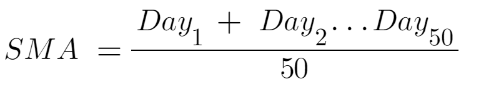

How to Calculate

The calculation for the 50-Day SMA is as follows:

Why It Might Be Useful

There are a number of common usages for an SMA, some of which I’ll cover in future episodes. For instance, an SMA cross can be used to indicate a market upturn or downturn.

Being able to plug these into your trading bot means that you can easily come up with more complex trading algorithms.

What You’ll Need

- Python 3

- Python Panda’s

- (useful) An IDE. I use Jetbrains Pycharm, link at the bottom

How To Do It

Retrieve Data from Binance

Retrieving data from Binance is relatively straightforward. Here’s how:

- Import the official Binance Python Connector

from binance.spot import Spot() - Add the following function:

# Function to query Binance for candlestick data

def get_candlestick_data(symbol, timeframe, qty):

# Retrieve the raw data

raw_data = Spot().klines(symbol=symbol, interval=timeframe, limit=qty)

# Set up the return array

converted_data = []

# Convert each element into a Python dictionary object, then add to converted_data

for candle in raw_data:

# Dictionary object

converted_candle = {

'time': candle[0],

'open': float(candle[1]),

'high': float(candle[2]),

'low': float(candle[3]),

'close': float(candle[4]),

'volume': float(candle[5]),

'close_time': candle[6],

'quote_asset_volume': float(candle[7]),

'number_of_trades': int(candle[8]),

'taker_buy_base_asset_volume': float(candle[9]),

'taker_buy_quote_asset_volume': float(candle[10])

}

# Add to converted_data

converted_data.append(converted_candle)

# Return converted data

return converted_dataCreate an SMA Calculator

The SMA calculator takes a given symbol, timeframe, and sma_size and returns a dataframe with all the SMA values added. This is incredibly simple with Pandas as we use the rolling function to group together the required number of observations.

Here are the steps the function walks through:

- Retrieve

raw_datausingget_candlestick_data(I’ve assumed the maximum of 1000 rows for this) - Convert

raw_datainto a dataframe - ‘Roll’ through the dataframe and calculate the mean

Here is the code for the function:

# Function to calculate a generic SMA

def calc_sma(symbol, timeframe, sma):

# Get the raw data

raw_data = get_candlestick_data(symbol=symbol, timeframe=timeframe, qty=1000)

# Convert into dataframe

df_data = pandas.DataFrame(raw_data)

# Create name for new column

name = "SMA_" + str(sma)

# Roll through the dataframe to get the SMA

df_data[name] = df_data['close'].rolling(sma).mean()

return df_dataHow to use

Now, in order to calculate the 50-day SMA, all you need to do is pass the values of the symbol=<your symbol>, timeframe="1d", and sma=50 and you’ll be all set.

Full Code

import pandas

from binance.spot import Spot

# Function to calculate a generic SMA

def calc_sma(symbol, timeframe, sma):

# Get the raw data

raw_data = get_candlestick_data(symbol=symbol, timeframe=timeframe, qty=1000)

# Convert into dataframe

df_data = pandas.DataFrame(raw_data)

# Create name for new column

name = "SMA_" + str(sma)

# Roll through the dataframe to get the SMA

df_data[name] = df_data['close'].rolling(sma).mean()

return df_data

# Function to query Binance for candlestick data

def get_candlestick_data(symbol, timeframe, qty):

# Retrieve the raw data

raw_data = Spot().klines(symbol=symbol, interval=timeframe, limit=qty)

# Set up the return array

converted_data = []

# Convert each element into a Python dictionary object, then add to converted_data

for candle in raw_data:

# Dictionary object

converted_candle = {

'time': candle[0],

'open': float(candle[1]),

'high': float(candle[2]),

'low': float(candle[3]),

'close': float(candle[4]),

'volume': float(candle[5]),

'close_time': candle[6],

'quote_asset_volume': float(candle[7]),

'number_of_trades': int(candle[8]),

'taker_buy_base_asset_volume': float(candle[9]),

'taker_buy_quote_asset_volume': float(candle[10])

}

# Add to converted_data

converted_data.append(converted_candle)

# Return converted data

return converted_dataSay Hi!

I love hearing from my readers, so feel free to reach out. It means a ton to me when you clap for my articles or drop a friendly comment — it helps me know that my content is helping.

❤